The famous Spanish writer Miguel Cervantes arguably invented the well-known proverb:

Don't put all your eggs in one basket.

BHP Billiton (BBL) (BHP) follows this proverb in spirit, which is intended to protect an investor from risk of business failure. Broadly, BBL leverages from a well-diversified portfolio of operations in terms of underlying commodity as well as in terms of location. BBL is also a good investment in terms of divided due to the fact that it generates a dividend yield of around 4%. However, the major risks facing BBL are the exchange rate (the mining costs have to be paid in local currency, which, if grows strong against the US dollar, causes the dollar-denominated costs to rise and profits to shrink), low commodity prices (resulting in lower sales) and the business environment (includes problems in managing relationships with the mine workers and their unions).

These are the general pros and cons for a well diversified, major market player like BHP Billiton. However, in this article, I will drill down into these broad risks and discuss at length how these risks may affect particular business segments of BBL going forward.

[Note: The terms BBL and BHP both refer to BHP Billiton and can be used interchangeably.]

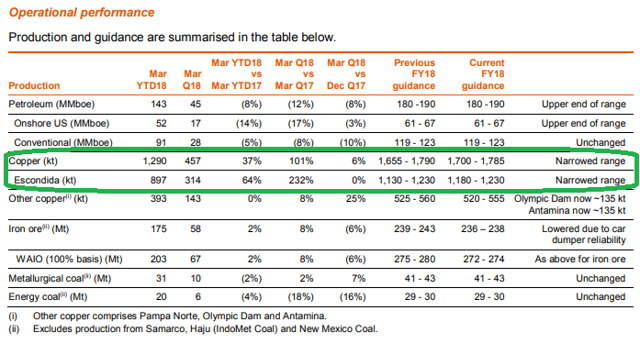

Billiton is mining copper with risks:When it comes to copper production, BBL has yielded impressive operating results during the 3Q 2018. BBL's largest copper stake in terms of underlying resource, the Escondida mine where it owns a 57.5% interest, has delivered a great quarter with 457 kt (read: '000 tonnes) of copper ore production, thereby leading to an increase of 101% YoY.

Source: BHP Operational Performance Review

As seen in the picture above, this led to a healthy 1,290 kt of production during the 9-month period ending this quarter, up 37% YoY. Increased volume was attributable to the fast-paced development at the Los Colorados Extension project at Escondida. Additionally, copper produced from other projects stood at 143 kt during the 3Q, up 25% QoQ. These projects included Pampa Norte and Antamina (both located in Chile) and the Olympic Dam (located in Australia). BBL will also benefit from cash inflows of approximately $320 million in 4Q 2018 that will accrue when it finalizes the deal to sell the Cerro Colorado copper mine in Chile.

Moreover, after considering the full FY 2018 guidance for all the copper mines operated by BHP, we can expect another round of solid copper production ranging between 410-495 kt during 4Q 2018.

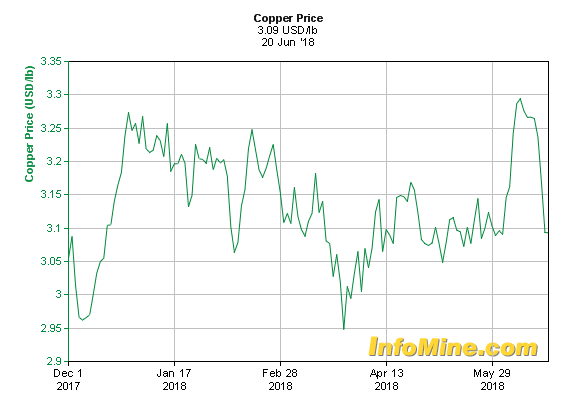

The risks facing Billiton's copper segment:However, the problem lies with the international copper prices which have been quite volatile during the past six months and currently stand near $3.09/lb. The copper prices have tumbled among fears of an impending trade war between the US and China, following the US threat to impose a 10% tariff on $200 billion worth of Chinese goods. In my view, such threats are less likely to materialize and copper prices may stabilize in the near future, thereby improving sales volume attributable to the segment.

Source: Infomine

Another problem which looks more significant to me is the issues raised by the union of workers at the Escondida mine. The union has demanded 5% increase in workers' salaries along with a bonus payment of approximately $34,000 per worker. The negotiations are underway and expected to settle in the coming one month or so. In my view, this time period is important because if BHP decides to accept the demands set forth by the union, then this would significantly impact the cost of production and also result in a heavy one-time cash outflow. To assess the significance of the problem, it is noteworthy that a previous strike called by mine workers' union resulted in a loss of approximately $1 billion for BHP, in terms of production.

Billiton's Iron Ore Operations and Risks therein:BBL produced approximately 58 Mt (read: Million tons) of iron ore during 3Q, up 8% YoY but down 6% on a QoQ basis. Due to unplanned car dumper maintenance, BBL had to reduce the FY guidance from the previous range of 239-243 Mt to the revised range of 236-238 Mt of ore. Although BBL's iron ore operations comprise of the Samarco mine (Brazil) and the WAIO (read: Western Australian Iron Ore) operations, only the latter project is delivering production.

BBL is currently facing problems in managing the Samarco operations, a joint venture between BBL and Vale S.A (VALE), because the operations are suspended following a failure in the tailings dam that flooded nearby areas and killed 19 people and caused environmental damage back in 2015. Since then BBL is facing legal consequences which are expected to result in cash outflows of approximately $54 billion for the business partners. Consequently, BBL is trying to sell its 50% stake in the Samarco mine to VALE.

To compensate for the lost iron ore production at its Brazil operations, BBL is now looking for other more profitable projects elsewhere. In this context, it should be noted that BBL recently approved the development of South Flank operations in Western Australia at a cost of approximately $2.9 billion, in an attempt to replace depleting iron ore deposits. This move is expected to bring an additional 80 Mt when the project starts production in 2021 and will help improve the segment's cash flows going forward.

Concerns about Billiton's petroleum sector:As shown in the operational performance chart in an earlier section, BBL has produced a total of approximately 45 MMboe (read: Million barrels of oil equivalent) of petroleum products from its Onshore US and Conventional operations. The quarterly output was down 12% YoY and 8% QoQ. Moreover, given the fact the BBL has not revised the FY 2018 guidance which stands at ~180-190 MMboe of petroleum production, we can assume the 4Q production to lie within range of ~37-47 MMboe.

[Note: In this discussion, the term petroleum refers to crude oil, condensate and natural gas liquids.]

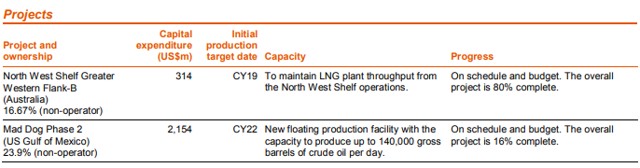

BBL has also acquired rights to explore some resource-rich petroleum projects, including the North West Shelf and Mad Dog, which are expected to incur CAPEX of ~$2.5 billion and expected to initiate output from FY 2019 onwards.

Source: BHP Operational performance review

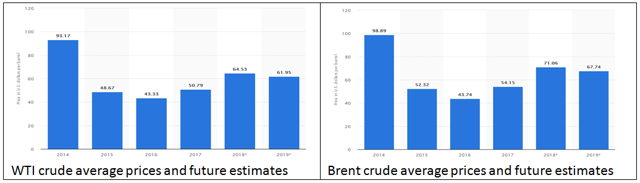

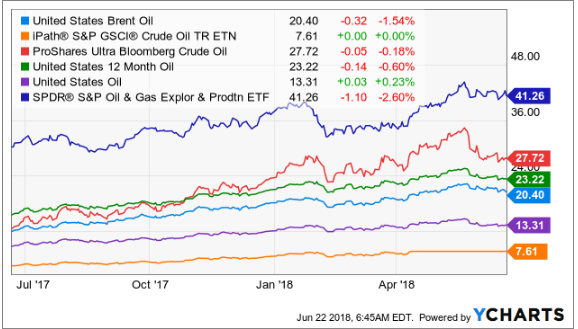

Oil Price Outlook is the main problem:However, I think the main problem for BBL is not a deficit in production, rather the oil prices that have tumbled during the past and affected BBL's revenues from this high-potential segment. Have a look at the oil chart below which represents the 6-month price fluctuation in the Brent and WTI (West Texas Intermediate) crude oil spot prices:

Source: Ycharts

Although the crude oil prices have improved since February, they are struggling to find support since mid of May 2018. Moreover, Statistica estimates that average prices for Brent and WTI in FY 2019 are expected to remain lower than the current year.

Source: Statistica

I think that the anticipation of reduced oil prices in the future is supported by the fact that many major oil ETFs are currently performing better with a general upward trajectory. My analysis includes the US Oil ETF (USO), the iPath S&P Crude Oil Total Return Index ETN (OIL), the ProShares Ultra Bloomberg Crude Oil ETF (UCO), the US Brent Oil ETF (BNO), the US 12 month Oil ETF (USL) and the SPDR S&P Oil and Gas Exploration & Production ETF (XOP).

At this point, it is appropriate to establish the supposedly inverse relationship between oil spot prices and performance of future-linked ETFs. ETFs frequently trade in oil future contracts and make gains. The dynamics of the transaction are such that when the existing future-sell contracts expire, ETFs close out their positions by simultaneously initiating a future-buy contract. At the time of close out of positions, if the market is expecting a decline in oil prices, then the ETF can forward-buy at a cheaper rate. This provides them with lucrative profits and consequently results in an increase in price as witnessed in the graph above.

Oil price decline and OPEC's role therein:In my opinion, the main element that may cause a decline in spot prices of crude oil is an anticipated increase in supply from OPEC countries. At present, the daily production of crude oil stands near 81.6 MBPD (read: Million Barrels Per Day), and the OPEC countries have proposed to increase oil production by 1 MBPD. If this proposal is accepted by the member nations, then it would push Brent crude prices further down and within range of $70/barrel.

Given the above discussion, it is easy to comprehend how BBL and other oil producing companies could suffer from shredded oil prices following an increase in OPEC supply which would be unmatched by an equivalent increase in demand. This is likely to reduce the segment's cash flows and affect sales in the coming quarters.

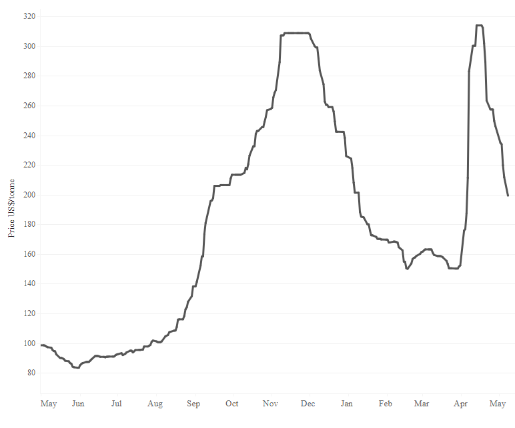

Billiton's coal segment is going fine:During 3Q 2018, BBL produced 10 Mt (read: million tons) and 6 Mt of metallurgical and energy coal, respectively, up 7% and down 16% QoQ. The increased output in metallurgical coal was mainly attributable to stabilized operations at Blackwater operations in the Queensland coal district (Australia). Have a look at the declining price trends of metallurgical coal that indicates BBL may have to face declining cash flows going forward.

Source: Metallurgical coal price by mining.com

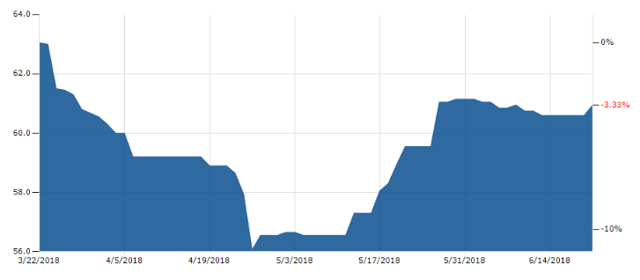

On the other hand, production decline in energy coal is mainly attributable to bad weather in the New South Wales mine in Australia and a higher strip ratio in Cerrej贸n mine in Colombia. However, as full-year guidance remains intact between 29-30 Mt; the 4Q is likely to yield greater output QoQ within range of 9-10 Mt. Once again, by looking at the price chart of energy coal, we can identify that energy coal price is rallying, and if the momentum can continue, then BBL may see increased cash flows and improved earnings going forward.

Source: Energy coal price by BusinessInsider.com

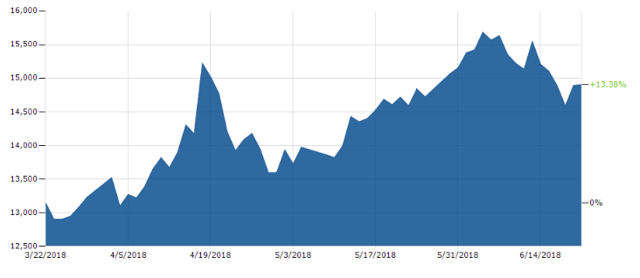

Billiton looks forward to restructure business operations:Deutsche Bank has estimated BBL's mine-to-market nickel business represented by the Nickel West mine in Western Australia to be worth approximately $690 million and this segment is BBL's only asset to retain its share in the EV (read: electric vehicle) industry. However, BBL recently indicated its plan to restructure the business operations by finding a suitable buyer for this business segment.

Source: Nickel price chart by BusinessInsider.com

Nickel trades in excess of $14,500 per ton and in my view BBL will lose handy cash flows if it decides to dispose off this business segment. I say so because the EV market is expected to reach $4 billion by the next 10 years or so, and BBL can leverage on increasing cash flows in a booming industry.

Conclusion:Based on the preceding discussion, I can figure out both risk factors and support factors in BBL's diversified operations. However, I believe that at present, the positive outlook from one segment is largely offset by a negative outlook in another segment, which is why BHP Billiton is less likely to see a significant share price appreciation in the near term. Nevertheless, BBL is a solid investment case that has a couple of upcoming potential projects which could bring increased cash flows and earnings in future.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.